HSA HDHP Limits Increase for 2026

On May 1, 2025, the IRS released Revenue Procedure 2025-19 to provide the inflation-adjusted limits for health savings accounts (HSAs) and high-deductible health plans (HDHPs) for 2026. The IRS is required to publish these limits by June 1 of each year.

These limits include the following:

- The maximum HSA contribution limit;

- The minimum deductible amount for HDHPs; and

- The maximum out-of-pocket expense limit for HDHPs.

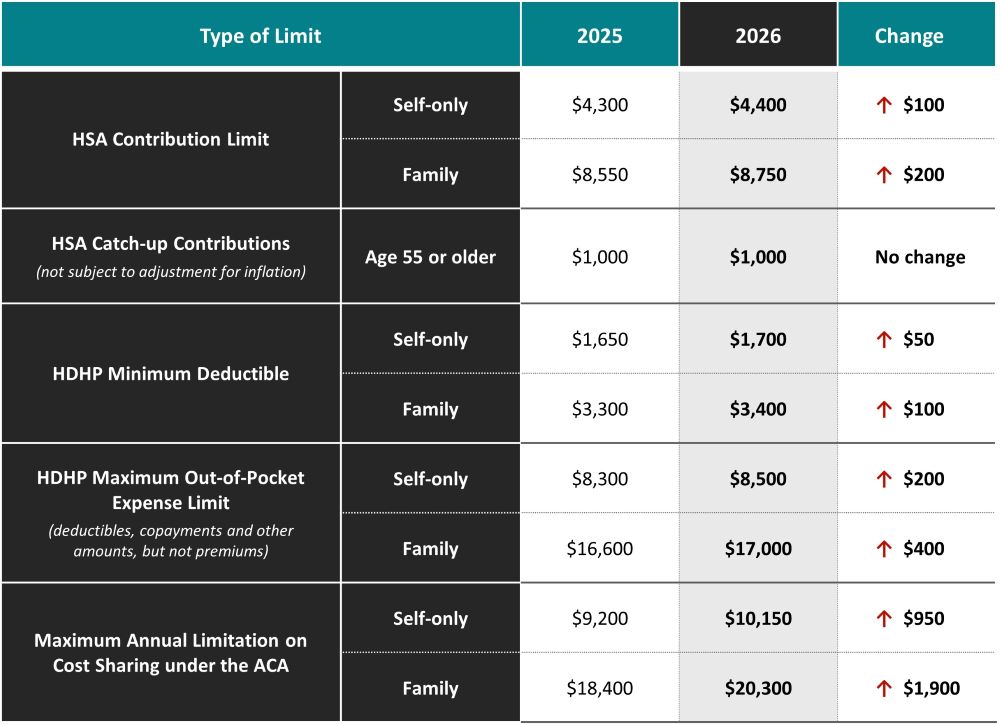

These limits vary based on whether an individual has self-only or family coverage under an HDHP. Eligible individuals with self-only HDHP coverage will be able to contribute $4,400 to their HSAs for 2026, up from $4,300 for 2025. Eligible individuals with family HDHP coverage will be able to contribute $8,750 to their HSAs for 2026, up from $8,550 for 2025. Individuals age 55 and older may make an additional $1,000 “catch-up” contribution to their HSAs.

The minimum deductible amount for HDHPs increases to $1,700 for self-only coverage and $3,400 for family coverage for 2026 (up from $1,650 for self-only coverage and $3,300 for family coverage for 2025). The HDHP maximum out-of-pocket expense limit increases to $8,500 for self-only coverage and $17,000 for family coverage for 2026 (up from $8,300 for self-only coverage and $16,600 for family coverage for 2025).

HIGHLIGHTS

- Each year, the IRS announces inflation-adjusted limits for HSAs and HDHPs.

- By law, the IRS is required to announce these limits by June 1 of each year.

- The adjusted contribution limits for HSAs take effect as of Jan. 1, 2026.

- The adjusted HDHP cost-sharing limits take effect for the plan year beginning on or after Jan. 1, 2026.

IMPORTANT DATES

January 1, 2026

The new contribution limits for HSAs become effective.

2026 Plan Years

The HDHP cost-sharing limits for 2026 apply for plan years beginning on or after Jan. 1, 2026.

HSA/HDHP Limits

The following chart shows the HSA and HDHP limits for 2026 compared to 2025. It also includes the catch-up contribution limit that applies to HSA-eligible individuals age 55 and older, which is not adjusted for inflation and stays the same from year to year.

ACTION STEPS

Employers sponsoring HDHPs should review their plans’ cost-sharing limits (i.e., the minimum deductible amount and maximum out-of-pocket expense limit) when preparing for the plan year beginning in 2026. Also, employers allowing employees to make pre-tax HSA contributions should update their plan communications with the increased contribution limits.

Contact a SSG Benefits Advisor for more information.

Prev

Prev